A Clear Account Reconciliation Example Step by Step

Think of account reconciliation as your financial reality check. At its most basic, it’s the process of taking your internal records for an account—let's say your cash account—and comparing them line-by-line against the statement from your bank. The goal is simple: find any differences and figure out why they exist.

This routine check ensures the cash balance you think you have is the cash balance you actually have. It’s how you spot things like checks that haven't been cashed yet or bank fees you might have missed.

What Is Account Reconciliation Really?

Here's a good analogy: imagine you and a friend both kept a running tab of money you owe each other. At the end of the month, you’d sit down, compare your notes, and make sure everything matches up. That's exactly what account reconciliation is in a business context. You're simply matching your internal financial records against an external, third-party statement, whether it's from a bank, a supplier, or a credit card company.

This isn't just about catching typos or small mistakes. It's a fundamental health check for your finances. When you reconcile your accounts regularly, you build a solid system of checks and balances that proves your financial data is both accurate and complete.

The Core Purpose of Reconciliation

Deep down, reconciliation answers one crucial question: Do the numbers in our books match reality? It’s your best line of defense against all sorts of financial headaches.

A disciplined reconciliation process helps you:

- Ensure Financial Accuracy: It confirms that the balances in your general ledger are correct and trustworthy, which is the bedrock of reliable financial reporting.

- Prevent and Detect Fraud: Unexplained differences can be the first red flag for unauthorized transactions or other fraudulent activity.

- Improve Cash Management: Knowing your precise cash balance is essential for making smart decisions about paying bills, budgeting for the future, and investing.

- Maintain Audit Readiness: Clean, well-documented reconciliations create a clear paper trail, which makes any future audit a much smoother and less stressful experience.

This process provides a clear, reliable picture of your company's cash flow and financial standing, turning confusing numbers into confident decisions. Without it, you’re essentially flying blind, hoping your financial statements are correct rather than knowing they are.

Why It Matters More Than Ever

As business gets more complex, the need for careful reconciliation only grows. There's a global push for greater financial transparency, and unfortunately, the threat of fraud is always present. These pressures are leading more companies to adopt stronger reconciliation habits and invest in better tools.

In fact, the U.S. reconciliation software market is expected to hit USD 1,331.8 million by 2032 as more businesses look for ways to cut down on manual work and meet strict reporting standards. You can explore more about these market trends and their drivers.

Here is the rewritten section, designed to sound more human and natural:

The Different Types of Reconciliation You Will Encounter

Account reconciliation isn't a one-size-fits-all task. It’s more like a set of specialized tools, each designed for a specific job. You wouldn't use a screwdriver to hammer a nail, and similarly, the records you compare will depend entirely on which part of your business you're trying to validate.

Getting a handle on these different types is fundamental to keeping your company’s financial health in check. Each one acts as a critical checkpoint for a specific area, from the cash flowing through your bank account to the money you owe your suppliers.

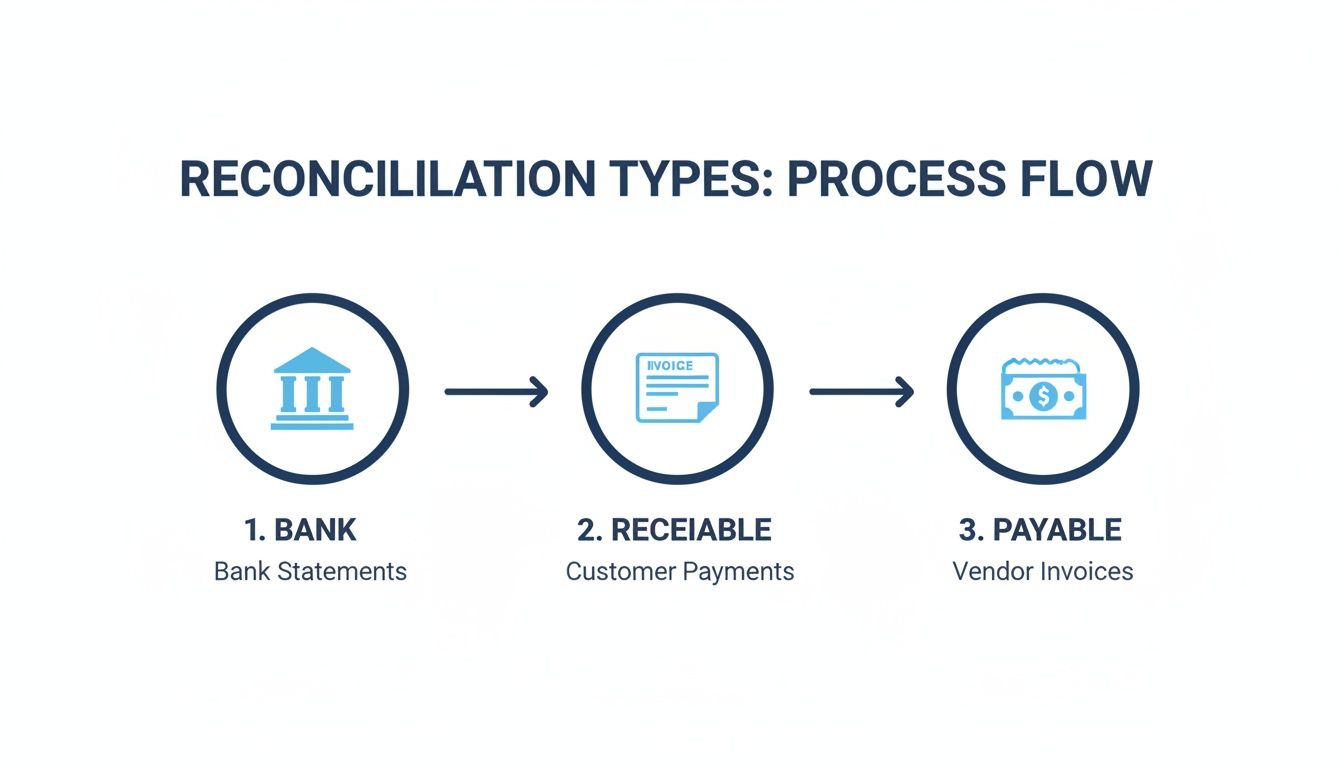

Bank Reconciliation

This is the one everyone knows, and for good reason—it’s the bedrock of financial accuracy. A bank reconciliation is simply the process of matching the cash balance in your books (your general ledger) with the cash balance shown on your bank statement. The whole point is to hunt down and explain any discrepancies.

Most of the time, the differences come down to timing. You might have checks you’ve sent out that haven't been cashed yet (outstanding checks), or deposits you made yesterday that are still processing (deposits in transit). Nailing this process ensures your cash records are spotless, which is the foundation for pretty much all other financial reporting.

Accounts Receivable and Payable Reconciliation

These two are all about managing the money flowing in and out of your business—critical for keeping cash flow healthy and relationships with customers and vendors strong.

- Accounts Receivable (AR) Reconciliation: Here, you’re matching your detailed list of unpaid customer invoices (the AR aging report) to the summary AR balance in your general ledger. This confirms you know exactly who owes you what, which is essential for chasing down late payments and accurately forecasting the cash you have coming in.

- Accounts Payable (AP) Reconciliation: On the flip side, this process matches your list of unpaid vendor bills (the AP aging report) with the main AP account in your ledger. It’s your best defense against accidentally paying a bill twice or missing a payment deadline with a key supplier.

A regular reconciliation habit for both AR and AP is absolutely non-negotiable for anyone serious about cash flow forecasting. It gives you clear answers to two of the most important questions in business: “How much money is coming in?” and “How much has to go out?”

Advanced Reconciliation Types

As a business gets bigger, its finances get more complicated, and that calls for more specialized checks and balances. Two of the most common are intercompany and payroll reconciliations.

An intercompany reconciliation is a must for any company with multiple subsidiaries or divisions. It’s all about matching transactions between these related entities to make sure their internal accounts cancel each other out. This process strips out any "internal profits" from the consolidated financial statements, giving you a true picture of the company's performance with the outside world.

Finally, payroll reconciliation ensures what you think you paid your employees is what you actually paid. It compares the wages, taxes, and deductions from your payroll system against the cash that actually left your bank account and was sent to the tax authorities. This helps you catch costly mistakes before they turn into major headaches. Each account reconciliation example plays a unique role, but together, they form a web of controls that protects your company’s financial integrity.

Let's Walk Through a Bank Reconciliation Example

Theory is one thing, but rolling up your sleeves and actually doing a reconciliation is where it all clicks. Let's follow a small business, "Creative Crafts Co.," as they reconcile their cash account for the month of July. This real-world account reconciliation example will show you exactly how to tackle common discrepancies like uncashed checks and surprise bank fees.

The whole process kicks off with two key documents: the company's internal cash ledger for the month and the official bank statement for that same period.

Step 1: Gather Your Documents

First things first, we need our starting points. At the end of July, Creative Crafts Co.'s internal cash book shows a balance of $4,550. A few days later, the bank statement arrives, but it shows a different number: $5,185.

Don't panic! A difference like this is completely normal. Our job now is to investigate and pinpoint the exact items that explain the $635 gap between their books and the bank's records.

Step 2: Compare and Match Transactions

Next, it's time to play detective. We'll go line-by-line, comparing every deposit and withdrawal in the company's ledger against the bank statement. Think of it like checking two different shopping lists for the same trip—we're looking for what's on one list but missing from the other.

After a careful review, the bookkeeper at Creative Crafts Co. finds a few discrepancies:

- Deposits in Transit: A $500 deposit made on July 31st is recorded in the company’s books, but it hit the bank too late to appear on the July statement.

- Outstanding Checks: Two checks they wrote in July haven't been cashed yet by the vendors. These are Check #121 for $200 and Check #124 for $75.

- Bank Service Charges: The bank quietly deducted a $20 monthly maintenance fee. The company only found out about it from the statement.

- Interest Earned: On the bright side, the bank paid $10 in interest on the account balance—another item the company's books don't reflect yet.

This process of comparing internal documents to external ones is the heart of reconciliation, no matter the account type.

As you can see, whether you're dealing with cash, customer payments, or vendor bills, the core idea is always the same: match your records to an outside source. For a deeper dive into this specific process, check out this a detailed guide on bank reconciliation.

Step 3: Prepare the Reconciliation Statement

Now for the main event: building the reconciliation statement. This isn't just a simple list; it's a two-sided calculation. We'll adjust the bank balance and the book balance separately, with the goal of making them meet at a single, correct number.

Adjusting the Bank Balance

Let's start with the bank's number. We need to account for the transactions that have already happened but that the bank doesn't know about yet.

- Start with the Bank Statement Balance: $5,185

- Add Deposits in Transit: + $500 (This cash was received but not yet processed by the bank.)

- Subtract Outstanding Checks: - $275 (The bank doesn't know this money is already spent.)

After these adjustments, the Adjusted Bank Balance comes out to $5,400.

Adjusting the Book Balance

Next, we'll turn to the company's cash ledger. We need to update it for the items we just discovered on the bank statement. To see more about how to structure this, our guide on preparing a bank reconciliation statement is a great resource.

- Start with the Book Balance: $4,550

- Add Interest Earned: + $10 (Good news—the company has more cash than it thought.)

- Subtract Bank Fees: - $20 (This fee needs to be recorded as an expense.)

But wait. A quick calculation ($4,550 + $10 - $20) gives us $5,440. It doesn't match the bank's adjusted balance of $5,400.

This is a classic reconciliation roadblock! A $40 difference means we missed something. The bookkeeper digs back into the records and finds the culprit: Check #121, which was paid to a supplier, was for $240, not $200. It was a simple typo in the cash ledger.

Let's fix the calculation for outstanding checks on the bank side.

- Corrected Outstanding Checks: $240 (Check #121) + $75 (Check #124) = $315

Now, let's recalculate the adjusted bank balance:

- $5,185 (Bank Balance) + $500 (Deposit) - $315 (Corrected Checks) = $5,370

And update the book balance with the check error:

- $4,550 (Book Balance) + $10 (Interest) - $20 (Fee) - $40 (Check Error) = $5,500

Still no match. This is frustratingly common, but it's why we reconcile—to find every last error. After one last look, the bookkeeper finds another typo: the starting book balance of $4,550 was keyed in wrong. The correct balance from the prior month's reconciliation was $4,420.

Let's try this one last time with all the correct numbers.

Bank Side Adjustments:

- Start with Bank Balance: $5,185

- Add Deposits in Transit: + $500

- Subtract Outstanding Checks: - $315

- Final Adjusted Bank Balance: $5,370

Book Side Adjustments:

- Start with Correct Book Balance: $4,420

- Add Interest Earned: + $10

- Subtract Bank Fees: - $20

- Subtract Check Recording Error: - $40

- Final Adjusted Book Balance: $4,370

Even with all that, they still don't match. This example, with its messy, real-world errors, proves just how critical careful data entry is. Let's reset with a cleaner, final scenario to show what a successful reconciliation looks like.

A Successful Reconciliation

Imagine the initial numbers were slightly different:

- Bank Balance: $5,630

- Book Balance: $5,425

And the reconciling items were:

- Deposits in Transit: $300

- Outstanding Checks: $505

- Bank Service Charge: $15

- Interest Earned: $25

Here’s the final reconciliation statement that makes everything balance perfectly.

Sample Bank Reconciliation Statement

This table illustrates how we adjust both balances to arrive at the same true cash position.

| Bank Balance Adjustments | Amount | Book Balance Adjustments | Amount |

|---|---|---|---|

| Balance per Bank Statement | $5,630 | Balance per Books | $5,425 |

| Add: Deposits in Transit | $300 | Add: Interest Earned | $25 |

| Less: Outstanding Checks | ($505) | Less: Bank Service Charge | ($15) |

| Adjusted Bank Balance | $5,425 | Adjusted Book Balance | $5,425 |

Success! Both sides match at $5,425. The final step is for the bookkeeper to record journal entries for the bank charge and the interest earned. This officially updates the company's ledger to the correct, reconciled cash balance.

Navigating Common Reconciliation Roadblocks

Sooner or later, every accountant hits a wall during reconciliation. A number refuses to match, a transaction seems to have vanished into thin air, and the frustration starts to build. This is a completely normal part of the process, and knowing what to look for makes troubleshooting a whole lot easier.

These aren't just small hiccups; they're genuine risks. With so many payment methods and a constant flow of data, manual reconciliation can feel like trying to build a house of cards in a wind tunnel. Plus, companies are under more pressure than ever to keep perfect financial records. When you're dealing with huge transaction volumes, even small mistakes can snowball into big problems, as you can discover in this analysis of financial reconciliation challenges.

Let's look at the usual suspects.

Timing Differences

This is, by far, the most common and least scary issue you'll run into. Timing differences pop up when your company records a transaction in one accounting period, but the bank or vendor doesn't process it until the next one.

Here are a couple of classic examples:

- Outstanding Checks: You cut a check to a vendor and immediately record it in your books. But it won't actually clear your bank account until that vendor cashes it, which could be days or even weeks later.

- Deposits in Transit: You deposit a customer payment on the last day of the month and log it. However, the bank doesn't process it until the next business day, so it shows up on the following month's statement.

These aren't actual errors—they're just temporary mismatches that will sort themselves out. The trick is to identify them, note them clearly on your reconciliation, and then verify they clear in the next period.

Data Entry Errors and Missing Transactions

Ah, the classic human error. A simple typo, like keying in $95 instead of $59, can throw off your entire reconciliation and send you down a rabbit hole looking for the problem. These can be the most annoying issues to track down because the mistake could be anywhere.

Likewise, missing transactions can create imbalances that are tricky to find. Think about a small monthly bank fee, an automatic software subscription, or a little bit of interest earned. These often show up on the bank statement but are easy to forget to record in your own books. This is exactly why a meticulous, line-by-line comparison is so important.

For more complex accounts, a good format is your best friend. Have a look at our guide to find the perfect bank reconciliation statement template to keep everything organized.

Solution: The best defense is a good offense. Try a "buddy system" where a second pair of eyes reviews the reconciliation before it's finalized. You'd be amazed how many small mistakes this simple cross-check can catch.

For those recurring missing items like bank fees, just create a simple monthly checklist. By getting ahead of these common roadblocks, you can turn what feels like a stressful chore into a smooth and predictable routine.

How Automation Is Changing the Reconciliation Game

If you've ever spent hours manually ticking and tying numbers, you know the old way of doing reconciliations is just plain broken. It's not just tedious; it's a perfect setup for the exact kinds of human errors we’re trying to prevent in the first place. This is where technology finally gives us a real solution.

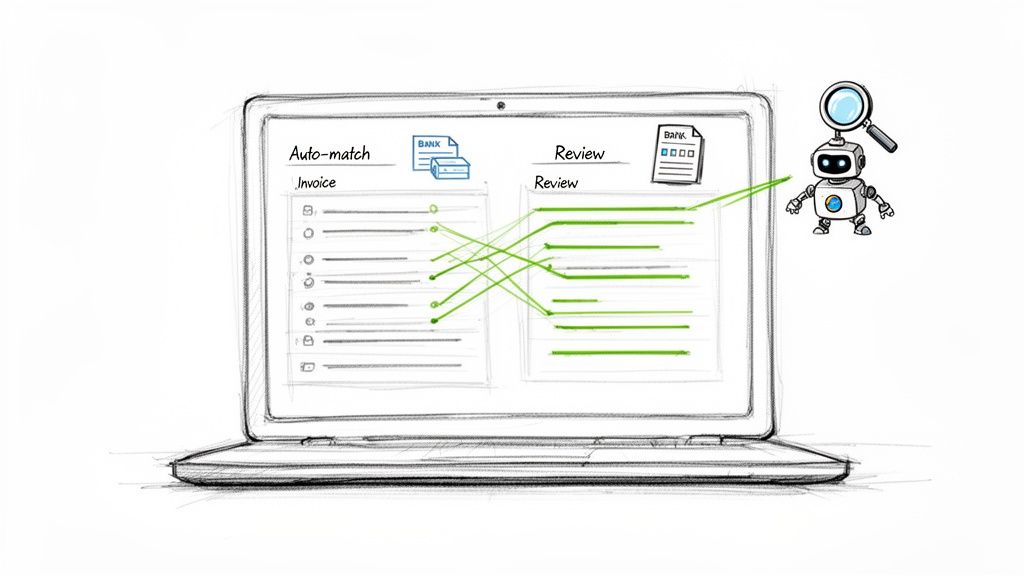

Think about it: software that can read your bank statements, pull data from supplier invoices, and line it all up against your general ledger automatically. These tools don't just see numbers and text; they understand the context. They grab dates, amounts, and invoice numbers and start matching them up before you've even had your morning coffee.

This isn't about replacing accountants. It's about shifting their focus from mind-numbing data entry to high-level analysis—letting them use their brains to investigate actual discrepancies, not hunt for typos.

The Power of Automated Matching

The real magic of automation is its ability to chew through huge volumes of transactions with incredible speed and accuracy. A human would lose their mind trying to compare thousands of line items, but software can knock it out in seconds, flagging only the items that need a second look. For any business with a high number of transactions, manual methods just can't keep up.

These systems use smart rules and algorithms to handle all kinds of matching scenarios:

- One-to-One Matching: The simple stuff, like matching a single payment to a single invoice.

- One-to-Many Matching: A bit trickier, like when one large customer payment covers several smaller invoices.

- Many-to-Many Matching: The really complex situations where multiple payments are reconciled against a batch of different invoices.

By handing these matching tasks over to software, finance teams have been known to cut their reconciliation time by over 90%. This isn't just about closing the books faster; it's about giving your finance experts time back to focus on strategic work that actually moves the business forward.

Beyond Speed: The Benefits of Accuracy and Control

Speed is great, but the boost in accuracy and internal controls is where automation really shines. It drastically reduces the risk of human error, which means the financial reports you rely on are built on a solid, trustworthy foundation. The future here is clearly heading toward more advanced tools, with AI automation completely changing how companies approach their financial close.

On top of that, automated systems create a perfect audit trail. Every single step, from importing a file to matching a transaction, is logged automatically. When auditors show up, they get a transparent, easy-to-follow record of the entire process, which makes their job (and yours) much simpler. With a full history of who did what and when, financial integrity stops being a goal and starts being a built-in feature of your process.

Ready to see how it works? You can learn more about getting started with automatic document processing and see these benefits for yourself.

Your Top Reconciliation Questions, Answered

Even after walking through the process, a few practical questions always seem to pop up. Let's tackle some of the most common ones I hear from business owners and bookkeepers so you can move forward with confidence.

How Often Should I Reconcile My Accounts?

The simple answer? It depends, but for most businesses, monthly reconciliation is the sweet spot. Doing it once a month is frequent enough to catch errors before they become massive headaches, but not so often that it feels like a constant burden.

If your business is humming with a high volume of daily transactions—think retail or e-commerce—you might want to step it up to weekly reconciliations. On the flip side, if an account sees very little action, you might get away with quarterly. The key isn't the exact frequency, but consistency. Whatever you choose, stick to it.

What Is the Difference Between Reconciling and Auditing?

This is a great question, and the distinction is important. Think of it this way: reconciliation is like you balancing your own checkbook at the kitchen table. It's a routine, internal process you perform to make sure your records are accurate.

An audit, on the other hand, is like having an independent inspector come in to verify your work. It's a formal, external examination of your financial statements by a professional to ensure they are fair and accurate for outside parties like investors, banks, or regulators.

What Do I Do If My Accounts Don't Balance?

First, take a deep breath. It happens to everyone. The first step is to double-check your own math—a simple addition error is often the culprit.

If it's still off, the size of the discrepancy is your best clue. Are you off by $50? Scan your bank statement for a $50 service fee you forgot to log. Is the difference divisible by 9? You might have transposed a number (e.g., typing 54 instead of 45).

Some of the most common reasons an account reconciliation example won't balance are:

- Bank fees or interest payments you haven't recorded yet.

- Checks you've sent out that haven't been cashed (outstanding checks).

- A simple typo during data entry.

Work through your entries methodically until you pinpoint the issue. Once you find it, a quick adjusting journal entry will set things straight.

With transactions becoming more complex, it's no surprise the global account reconciliation software market is expected to hit USD 6.15 billion by 2032. As businesses juggle more payment methods, tools that deliver over 99% matching rates are becoming a necessity, not a luxury. You can learn more about the growth of reconciliation software and why so many are making the switch.

Ready to stop wasting hours on manual reconciliation? DocParseMagic turns messy bank statements, invoices, and reports into clean, organized spreadsheets in minutes. Stop the tedious copy-paste and let our platform extract the data you need with perfect accuracy. Sign up for free and see how it works at https://docparsemagic.com