A Complete Bank Statement Example Explained for 2026

Think of a bank statement as the official story of your money for one month. It’s a detailed report card from your bank, showing every dollar that came in and every dollar that went out. This document is a critical piece of evidence for big financial moments, like applying for a loan or filing your taxes.

What Exactly Is a Bank Statement?

A bank statement is much more than just a list of transactions. It's a formal, legally recognized summary of your financial activity over a specific period—usually a month. This document acts as the definitive record of your account's health, detailing every single deposit, withdrawal, fee, and interest payment.

Unlike the real-time transaction history you see in your banking app, a statement is a static snapshot. It captures your opening and closing balances for the month, giving you a clear beginning and end point. This official format is precisely why lenders, accountants, and auditors rely on it for verification. You can learn more about the differences and best practices for managing online bank statements in our related guide.

Getting comfortable with its structure is the first real step toward mastering your finances. Every statement, regardless of the bank, contains the same core elements designed to give you a complete financial picture.

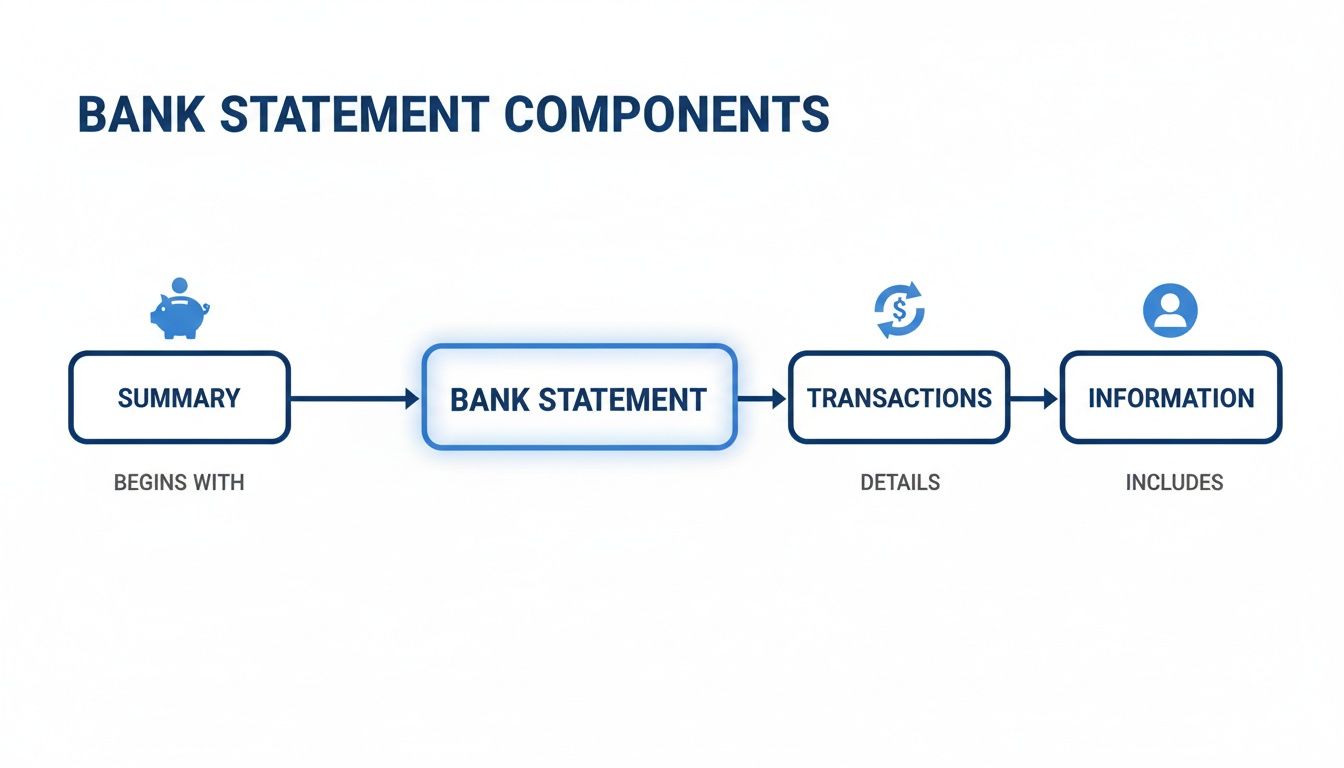

Key Components at a Glance

Before we dive into a detailed bank statement example, let's quickly break down the main sections you'll find. Each part tells a different piece of your financial story for the month.

This table gives you a quick rundown of the essential components.

Quick Guide to Bank Statement Sections

| Component | What It Tells You |

|---|---|

| Account Summary | A high-level overview, including your starting balance, total deposits, total withdrawals, and ending balance. |

| Personal Information | Confirms your name, address, and account number, ensuring the statement belongs to you. |

| Transaction Details | A chronological log of every debit (money out) and credit (money in) during the statement period. |

| Bank Information | Provides the bank’s contact details, which is crucial for inquiries or reporting discrepancies. |

Think of these components as chapters in your monthly financial narrative. The summary gives you the plot overview, while the transaction details provide the scene-by-scene action. Knowing how to read them all together gives you full control.

Breaking Down a Real Bank Statement Example

Theory is one thing, but getting your hands on a real bank statement is where it all starts to click. Think of it like learning to read a map—you can study the symbols all day, but you only really get it when you trace the route with your finger. That's exactly what we're about to do.

Below is a sample bank statement with all the key areas numbered. We'll walk through it together, section by section, so you know exactly what you're looking at and where to find the most important information.

You can see how this layout gives you the big picture right at the top before you dive into the nitty-gritty details below. It’s a pretty common design. Now, let’s unpack what each of these numbered sections really tells us.

The Header and Account Summary

The very top of the statement is your starting point. It's designed to quickly confirm who the statement belongs to and give you a high-level snapshot of the month's activity.

- Personal and Bank Information: This is the basic "who, what, and when." It includes your name and address, the bank's contact info, the statement date, and the statement period (the exact date range, like May 1, 2026 - May 31, 2026).

- Account Details: Right nearby, you'll find your account number (usually partially hidden for security) and what kind of account it is, such as "Total Business Checking." Always glance at this first to make sure you're even looking at the right document.

- The Account Summary: This is the 30,000-foot view of your money for the month. It's a simple, powerful formula:

- Beginning Balance: How much money you started with.

- Total Deposits/Credits: All the money that came in.

- Total Withdrawals/Debits: All the money that went out.

- Ending Balance: What you were left with after everything was settled.

This summary is often the first place a loan officer looks. It tells a quick story about your monthly cash flow without them having to wade through every single transaction.

Decoding the Transaction List

The real action happens in the transaction list. This is the heart of the statement—a chronological log of every single thing that happened with your money during that period. It’s where the numbers from the summary come to life.

Getting this part right is everything, especially for accounting. The global payments industry pulled in $2.5 trillion in revenue from 3.6 trillion transactions in just one year, with digital payments leading the charge. You can read more about these massive global payment trends on McKinsey.com. Every one of those transfers shows up as a line item right here.

Here’s a quick guide to the columns you'll almost always see:

- Date: The day the bank processed the transaction, which can sometimes be a day or two after you actually made the purchase.

- Description: This tells you a bit about the transaction—the name of the store, a check number, or a category like "ACH Payment" or "Point of Sale." For anyone who works with these documents regularly, our guide on how to read a PDF bank statement has some extra tips.

- Debits (-): This is all the money going out. Think of debits as subtractions from your balance. ATM withdrawals, debit card purchases, bills, and bank fees all live here.

- Credits (+): And this is all the money coming in—the additions to your balance. Things like a direct deposit from your job, a mobile check deposit, or a wire transfer are all credits.

Each line tells a tiny story. A debit at "The Daily Grind" is your morning coffee; a credit for "Payroll" is your paycheck landing. Following these entries line by line builds the complete picture of your financial life, which is the bedrock of good bookkeeping, budgeting, and financial planning.

Why Bank Statements Matter for Your Business

Think of a personal bank statement, and you probably just see a record of your spending habits. For a business, however, it's so much more. It’s the official story of your company's cash flow—a vital tool for growth, compliance, and day-to-day financial health. For any serious business owner, understanding its power isn't just helpful; it's essential.

In several high-stakes situations, this document is the primary evidence of your company's financial stability. Finance and operations teams who know how to read and manage them give their companies a serious advantage.

Most statements are broken down into a few core sections: the summary, the transaction list, and the general account information.

Each piece tells a part of your financial story, from the big-picture overview in the summary to the nitty-gritty details in the transaction log.

The Source of Truth for Loan Underwriting

When you apply for a business loan, lenders aren’t just going to take your word that you can pay it back. They need cold, hard proof of consistent income and responsible financial habits. Your bank statement is their go-to source for that proof.

Loan underwriters will pour over every line item. They're looking to verify your revenue claims, spot red flags like frequent overdrafts, and ultimately gauge your ability to take on new debt. A clean, well-managed statement paints the picture of a low-risk borrower, which can dramatically boost your odds of getting approved. In fact, having your statements ready is a key piece of any comprehensive mortgage documentation checklist.

Bedrock of Accurate Accounting

For your accountant or bookkeeper, the bank statement is the gospel. It's the final, authoritative record that all your internal books must align with. Every single transaction logged in your accounting software—from payroll runs to customer payments—has to match an entry on that statement.

This reconciliation process is what guarantees your financial reports, like the profit and loss statement and balance sheet, are actually accurate. Without it, you’re just guessing.

A reconciled bank statement provides an incorruptible audit trail. It confirms that your financial records are not just complete but are an accurate reflection of reality, which is essential for tax preparation and financial audits.

This has become more crucial as the volume of transactions explodes. In the first quarter of 2025 alone, global cross-border bank credit soared to a record $34.7 trillion. All of that capital is tracked on bank statements, which shows just how critical flawless document processing is in today's economy.

A Key Tool for Compliance and Fraud Prevention

Beyond getting loans and keeping clean books, bank statements are also a cornerstone of regulatory compliance. They are central to Know Your Customer (KYC) and Anti-Money Laundering (AML) checks.

Financial institutions rely on them to verify a business’s identity and confirm it's a legitimate operation, which helps them sniff out and prevent financial crime. By analyzing your transaction patterns, they can spot unusual activity that might signal fraud or other illegal dealings. For any business, being able to provide clear, accurate statements is fundamental to building and keeping a trusted financial reputation.

How to Spot a Fake Bank Statement

In our increasingly digital world, telling the difference between a real document and a clever fake is a critical skill. A fraudulent bank statement can be the key to loan scams, identity theft, and more. Think of it like learning how to spot a counterfeit bill—once you know what to look for, the forgeries become much easier to catch.

Most forgeries aren't built from scratch. It's far more common for someone to take a genuine bank statement example and just tweak a few things—a name here, a date there, or a few extra zeros on a deposit—using simple PDF editing tools. These small changes might seem minor, but they almost always leave a trail.

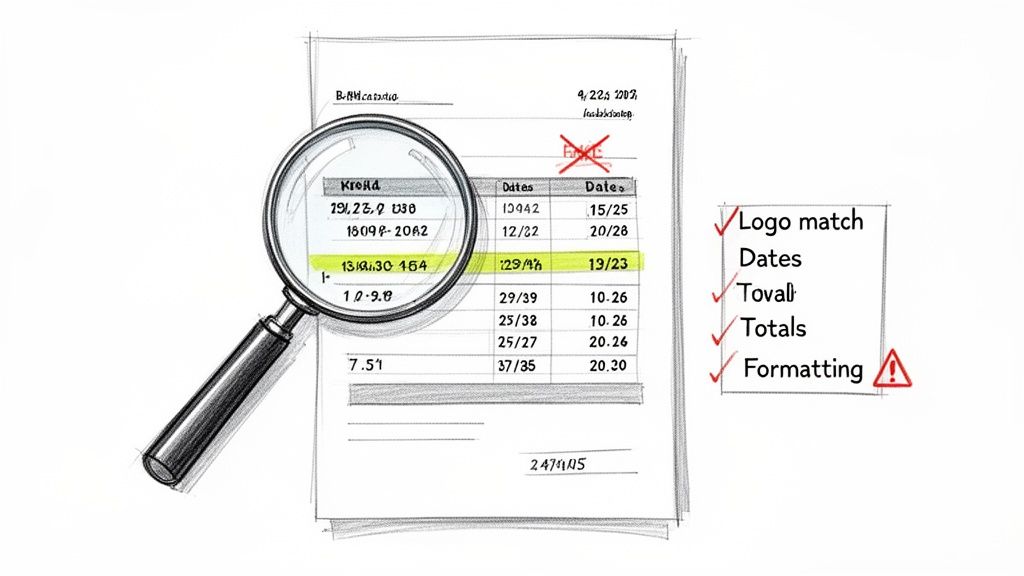

Visual Red Flags and Inconsistencies

Your first line of defense is a simple, careful visual inspection. Fraudsters often get sloppy with the little details that banks get right every single time because their systems are automated.

Keep an eye out for these tell-tale visual clues:

- Mismatched Fonts and Formatting: Banks are sticklers for consistency. Look for numbers or letters that seem just a bit off in size, style, or spacing. A single doctored number can stand out if you’re looking closely.

- Alignment Issues: Are the columns of numbers, dates, and text perfectly straight? When someone edits a line, it's often knocked slightly out of alignment with the rest of the document.

- Blurry or Low-Quality Logos: A real statement will have a sharp, high-resolution bank logo. If it looks fuzzy or pixelated, that’s a huge red flag. It usually means it was copied and pasted from a low-quality source.

- Generic Descriptions: Be wary of vague transaction details like "Deposit" or "Withdrawal" without any other information. Most banks provide much more specific memo lines.

A forger is counting on you to just give the document a quick glance. Your job is to slow down and really scrutinize the details they hope you'll miss.

Logical and Mathematical Errors

Beyond just looking wrong, fake statements often are wrong. They frequently contain logical gaps or math problems that a real bank statement would never have. These are much harder for a forger to get right because everything has to add up perfectly.

Double-check the document for these logical flaws:

- Incorrect Calculations: Take a calculator and manually check the math. Add a few deposits and subtract a few withdrawals to see if the running balance is correct. A single math error is all it takes to prove a statement is fake.

- Out-of-Sequence Dates: Transaction dates must follow a strict chronological order. If you see dates jumping around, it’s a dead giveaway that the document has been tampered with.

- Missing Official Elements: Every legitimate statement includes essentials like the statement period, a full account number, and the bank’s official contact information. If any of these are missing, be very suspicious.

At the end of the day, the only way to be 100% certain a statement is authentic is to confirm it directly with the bank that issued it. You can ask the person to share statements via a secure bank portal or, with their permission, contact the bank yourself to verify the document.

Stop Manual Data Entry with DocParseMagic

If you’ve ever found yourself hunched over a keyboard, manually typing numbers from a PDF bank statement into a spreadsheet, you know the feeling. It’s tedious. It’s slow. And frankly, it’s a waste of time that could be spent on actual analysis, not just mind-numbing transcription. This old-school approach to handling financial data is a major bottleneck for any growing business.

But what if there was a better way? Imagine dragging a folder filled with bank statements—from different banks, in different formats—into one place and getting a perfectly structured dataset back in moments. No more squinting at transaction lines or worrying about typos. That's the power of modern automation.

This isn’t just about saving a little time. It’s a fundamental shift that frees up finance professionals to focus on the high-value work they were hired to do.

From Document Chaos to Data Clarity

The biggest headache with any bank statement example is the format itself. PDFs are designed for people to read, which makes them a nightmare for software to understand consistently. DocParseMagic gets around this by using smart technology, like advanced Optical Character Recognition (OCR), to convert image to text using OCR and figure out the document’s layout.

The platform automatically identifies and extracts the crucial information, no matter how the bank designed the statement:

- Transaction Dates: It nails down the correct date for every single line item.

- Descriptions: It cleanly captures vendor names and other transaction details.

- Debits and Credits: Money in and money out are always separated accurately.

- Running Balances: It pulls the balance after each transaction happened.

DocParseMagic is built for the messy reality of financial documents. It can process dozens of different statement layouts without you ever needing to create or manage a single template.

This kind of power is critical. Between 2019 and 2024, the global banking system handled a staggering $122 trillion in funds. Think about the sheer volume of transactions behind that number. Automation isn't just a nice-to-have anymore; it's the only way to keep up.

The True Benefits of Automation

Making the switch to a tool like DocParseMagic pays off immediately. The most obvious win is the time you get back. A task that used to eat up hours of someone's day can now be finished in minutes.

This efficiency boost creates a more accurate and productive workflow across the board. You can see how this works in practice in our guide to streamlining banking document processing. By taking human data entry out of the equation, you virtually eliminate the risk of costly mistakes like typos or misplaced decimals. The end result is clean, reliable data you can confidently use for underwriting, bookkeeping, or financial reporting. It’s about turning that pile of documents into clear, actionable insights.

A Few Lingering Questions

Even after you get the hang of reading a bank statement, a few practical questions almost always come up. Let's tackle those common head-scratchers so you can handle these documents with confidence, no matter the situation.

Think of this as the final piece of the puzzle, moving you from just reading a statement to actually using it effectively.

How Long Should I Keep Bank Statements?

For your personal finances, a good rule of thumb is to hang onto your bank statements for at least one year. That gives you plenty of time to sort out any weird charges or just get a clear picture of your spending over the last 12 months.

But when it comes to business or taxes, the game changes. You'll want to keep those records for a minimum of three to seven years, depending on your local tax laws. And for anything tied to a major asset—think a mortgage or a business loan—it’s smart to keep those statements indefinitely. A secure digital folder is a great way to manage this without drowning in paper.

Can I Use an Online Statement for a Loan Application?

Yes, absolutely. Lenders and financial institutions are perfectly happy with the official PDF statements you download from your online banking portal. In fact, many actually prefer them since they're secure and much harder to fake than a paper copy.

The trick is to make sure you're providing the entire, multi-page document exactly as the bank generated it.

A quick screenshot of your recent transactions from your banking app won't cut it. Lenders need the full, official bank statement example with all the bells and whistles: the summary page, the bank's letterhead, and the complete transaction list.

When in doubt, just ask your lender what format they prefer before you hit send.

What Is the Difference Between a Bank Statement and a Transaction History?

This is a really important distinction. A bank statement is a formal, official document your bank creates for a specific period—usually one month. It’s a snapshot in time that’s considered a legal record, complete with summaries and official bank details, which is why it's used for things like loan applications and audits.

A transaction history, on the other hand, is the live, running list of debits and credits you see when you log into your banking app. It’s constantly changing and doesn't have the formal structure or official stamp of a proper statement. While it's great for checking your balance on the fly, it isn't accepted for anything that requires proof of your financial standing.

Stop wasting hours on manual data entry. DocParseMagic turns any bank statement into clean, organized data in seconds. Drag, drop, and you're done. Try it for free at DocParseMagic.